How to Price Products & Services

One of the most important decisions you will make in your business is setting prices for your products or services. The pricing strategy that you choose will influence customer expectations, so ensure that you can deliver. The most important factor when pricing is to ensure that you are covering your costs.

There are 5 common pricing strategies:

- Cost plus pricing – involves calculating your costs and adding a mark-up

- Competitive pricing or Market based– involves finding out what your competitors charge and setting a price based on how you compare. What your competitors are charging is always important to know.

- Value based pricing – Involves setting a price based on how much the customer believes what you’re selling is worth

- Price Skimming – involves setting a high price and lowering it as the market evolves. This is a pricing strategy used by tech firms who believe that early adopters want their product first so will pay a premium for it.

- Penetration pricing – involves setting a low price to break into a competitive market and raising it later.

This is usually used by startups and lowers their margin to increase sales volume however can be hard to keep customers once prices are lifted and normalised.

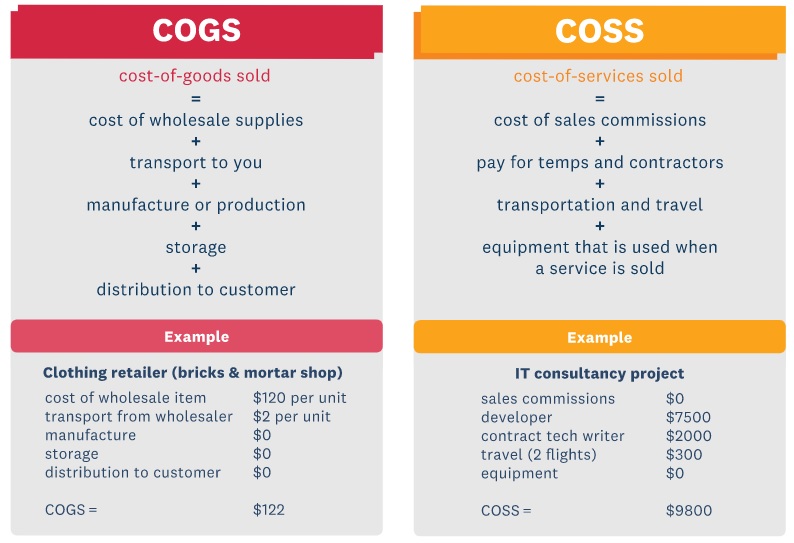

The first place to start when looking at pricing is to calculate your cost of goods sold (COGS) as the first rule of pricing is to sell for more than what you paid for your product.

Once you have calculated your COGS for each product you can look at the sales price. Your sales margin is the price minus COGS. Remember that the margin is not your profit there are still overhead expenses like stationary and utility bills that need to be paid and aren’t factored into your COGS. The margin that is required can vary between industries. A 5% product margin for businesses such as supermarkets can be highly profitable as they make so many sales whereas a restaurant or shop may require a 200% margin to be profitable.

Pricing factors

- Value Versus Cost – If the value your product or service provides to the customer is more than the cost to you. You are able to charge more for this. E.g. An accountant providing structure advice might cost them $700 however could charge $1,500 especially if this would save the client $10,000.

- Supply and Demand – if no one supplies the same product or service, you will be able to charge more until competition beings.

- Premium Pricing – Aim to price your brand as customers would expect to pay more for. E.g. Nike, Adidas, Apple etc

- Market Price – When selling everyday goods market price is very important to consider, if your prices are higher than other similar goods customers who are price sensitive will buy elsewhere. E.g. Supermarkets, if the same product is normally cheaper at Countdown or Pak n Save compared with New World you would usually shop at the better priced supermarket.

- Economy Pricing – You can aim to beat your competition on pricing however you will end up committing to very low margins. E.g. The Warehouse and Bunnings will price beat the competition if the same product is cheaper elsewhere.

Discounting

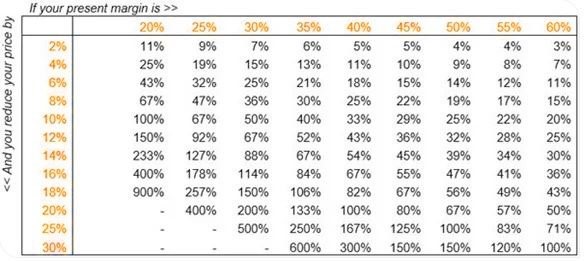

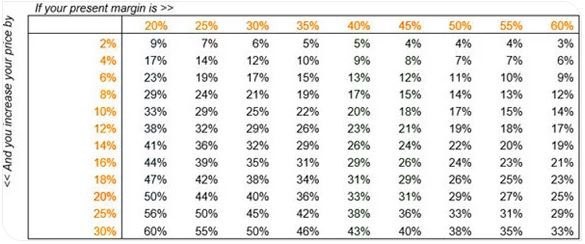

When competition increases it can be tempting to discount products and services however this can cause cashflow shortages for your business. Discounting should be considered as a tool to manage stock (especially if a product is slow moving) as this will provide a short term solution. E.g. If your product has a 25% margin, a 10% decrease in price would mean the sales volume would need to increase by 67% to maintain the same level of profit.

Premium Pricing

Raising your prices will have the opposite effect and decrease sales. Your product with a 25% margin, an increase of 10% could result in a sales reduction of 29%.

Consider the following when deciding on a pricing strategy:

1. Price – if you are going to compete on price this would lean towards a lower price, lower margin and higher volume strategy

2. Differentiation – to be the product leader would lean towards a higher price, higher margin and lower volume approach. Until competitors start to stock the same items.

3. Customer Experience – customisation and variation in products would also lean towards a higher price, higher margin and lower volume approach. This can be maintained as long as you continue to meet expectations for quality and value.

Your pricing strategy needs to match your target market. Pricing is one of the more important aspects of your marketing strategy. All pricing strategies can be a double edged sword. What can attract some customers can turn others off your product. You want customers to buy your product so it is important to use a strategy that is specific to your target market.